Global stock markets have taken a battering in 2022 over fears of high inflation, rising interest rates and the very real threat of an economic recession. US technology share prices have been hit particularly hard, with the tech-heavy Nasdaq Composite Index falling by more than 30% since November.

It was a similar story in Australia, albeit not quite as acute. Online stockbroking firm and Commonwealth Bank subsidiary, CommSec notes that in the financial year to 30 June, the Australian All Ordinaries index and S&P/ASX 200 fell by around 10 per cent after rising by around 25 per cent in the previous financial year.

As CommSec states, this sharemarket volatility was due to a multitude of factors, including war in Ukraine, supply chain disruptions, inflationary pressures, the lingering effects of a pandemic and a possible global recession.

Total returns on Australian shares (including dividends) fell by 7.4 per cent in the last financial year—a stark contrast to the previous year’s total rise of 30.2 per cent.

Australian Investors, fearful of a possible stock market crash, may be wondering how best to protect their investments during such a tumultuous time.

Here’s a look at what triggers such a collapse, what’s happened in the aftermath of previous large global crashes, the outlook for shares generally, and how investors can potentially protect their portfolios.

1. What is a stock market crash?

A stock market crash refers to a rapid, often unexpected, fall in share prices. Typically, this is defined as a drop of at least 10% on a stock exchange or major index in a day, or over a few days. A stock market crash may be temporary, with prices recovering in days or weeks. However, a crash can also signal the start of a longer downturn that can last for months, or even years.

Major stock market crashes in living memory include Black Monday (1987), the bursting of the dot.com bubble (2001-2002), the global financial crisis (2008-2009), and the COVID-19 pandemic (2020). The infamous Wall Street crash of October 1929 plunged the US into the so-called Great Depression lasting several years.

2. What causes a stock market crash?

A crash typically occurs at the end of a bull market, where share prices have risen for several years, and investors start to question whether companies have become overvalued. If investors start to sell shares as they believe share prices are unrealistic and will fall, this can trigger wide-scale panic selling. This creates a downward spiral of further share price falls as investors lose confidence in holding shares and hit the sell button.

Macro-economic factors can also play a role in triggering stock market crashes. In Australia, inflation rates are at their highest level in more than 20 years—as well as in the UK and the US—which has led to central banks increasing interest rates to curb inflation.

Rising interest rates tend to have a negative impact on stock markets for the following reasons:

- Valuations of ‘growth’ stocks: higher interest rates reduce the valuations of growth stocks, such as US technology firms, by decreasing the current value of future cash flows.

- Reduced consumer spending: companies may face reduced demand from consumers with less money to spend if the cost of debt increases, along with a rise in the cost of everyday items due to inflation.

- Relative return on savings: higher interest rates may encourage investors to move out of shares into cash-based products.

Australia has wound up its quantitative easing (QE) programme, and is moving into a phase known as ‘quantitative tightening’, or QT. The US and the UK are also winding up QE.

QE activity helped sustain share prices during the pandemic by stimulating economic growth. A tapering of this programme is likely to have a negative effect on the economy, leading to a more bearish market.

3. What happened after previous stock market crashes?

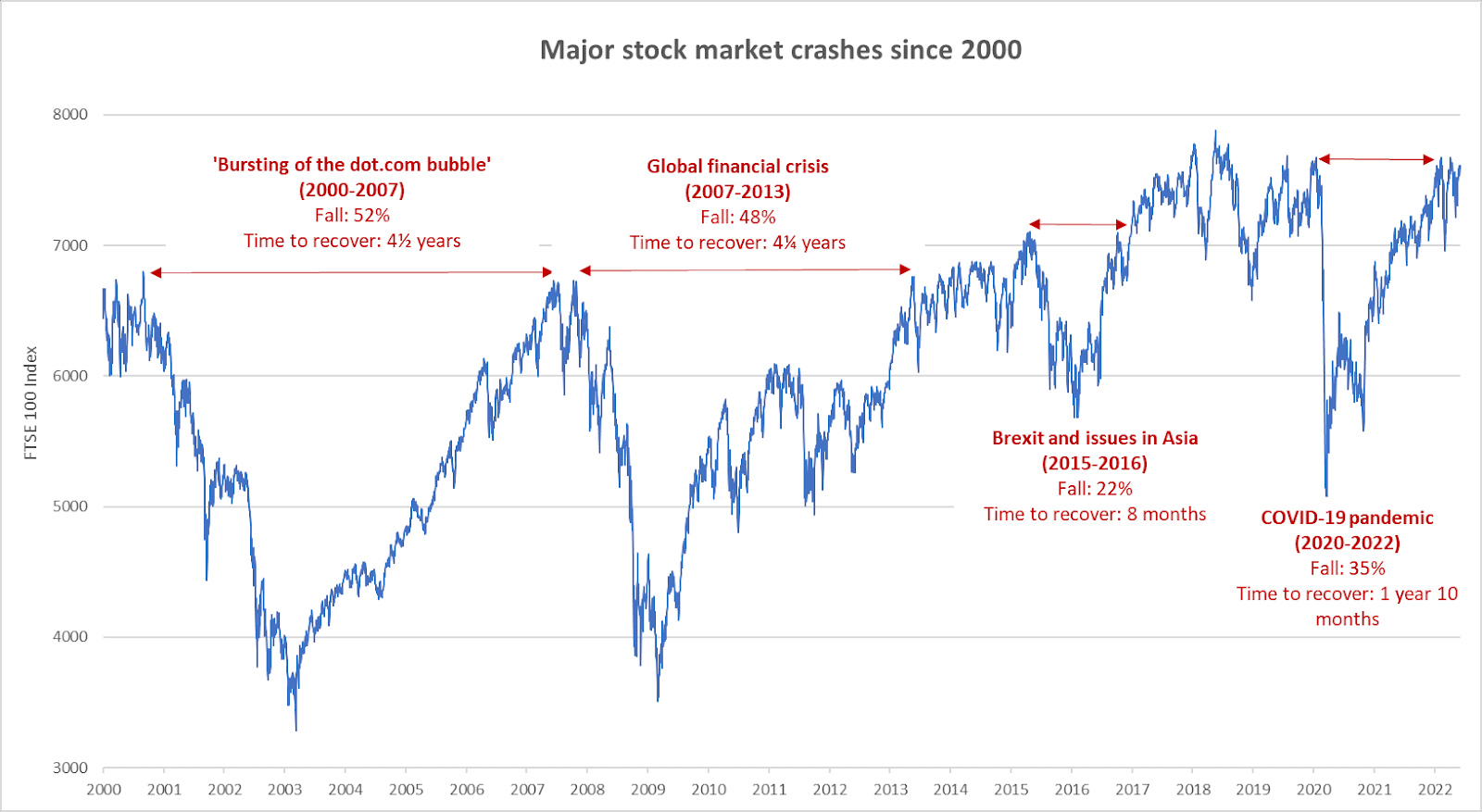

Investors naturally focus on how long stock markets have taken to recover after previous crashes. To provide some insight, the Forbes Advisor team analysed the major stock market crashes in the UK’s FTSE 100 since 2000:

Source of historical FTSE 100 data: WSJ Markets

While this data refers to London’s stock exchange, Australian investors can glean insights from some of the trends.

First, that the stock market is naturally cyclical, with, in the case of the FTSE, major falls of around 20% to 50% every eight to 10 years on average.

Unsurprisingly, the stock market has taken longer to recover from steeper falls, taking over four years to rebound from the 50% fall during the crashes caused by the dot.com bubble and the global financial crisis.

That said, more recent stock market falls have been shorter-lived, with the FTSE 100 recovering its pandemic losses within two years and within less than a year for the dip in 2015-2016.

Overall, the FTSE 100 has risen around 15% since 2000, although investors buying in at the bottom of the market in 2003 and 2009 would have doubled their money.

4. Should investors ‘buy on the dip’ or ‘sell in the fall’?

Considering the above graph, it may be tempting to try to sell investments before a crash and buy them back at lower prices just before the rebound. But, in reality, ‘buying on the dip’ is difficult to time, even for professional investors, with one trader advising Australian investors to give up the mantra entirely.

“I think all of us need to unlearn the ‘buy the dip’ mentality as that is a dangerous proposition in a falling market environment,” chief strategy officer of Tiger Brokers, Michael McCarthy, told ABC news.

While many investors may point to the gains they made under a ‘buying the dip’ strategy during the COVID-19 crash of March 2020, we are in a very different monetary policy environment in 2022: central banks are no longer pumping trillions of dollars into the economy and most are raising interest rates.

Russ Mould, investment director at AJ Bell, says history would suggest caution is needed when trying to beat the market: “No fewer than nine major rallies produced an average gain of 23% during technology stocks’ last major fall [in the global financial crisis] and all they did was expose buyers to a fresh mauling from a bear market as the Nasdaq plunged by 78%.”

Overall, investors taking a long-term view, rather than trying to ‘beat the market’, are able to smooth out their average returns.

According to a 2019 analysis by the Reserve Bank of Australia, Australian investors’ total return on equities, the sum total in other words of capital gains and dividends, is at around 10 per cent per year over the past 100 years based on a geometric average which allows for compounding over time. (Once inflation is taken into account, the average annual return was about 6 per cent).

“There have not been material differences in returns across sectors over this time, although of course there have been periods in which sectors have performed differently,” the RBA states.

Over a 10-year period, Australia’s central shares benchmark, the S&P/ASX 200 Index, has an average total return of 9.3% each year, according to the ASX’s investor update in 2021.

5. How to protect against a stock market crash

There is widespread pessimism about the near-term outlook for global markets. Experts fear further falls are likely, if not inevitable, in a difficult economic climate.

If inflation proves more stubborn than hoped, requiring higher interest rates for longer, then markets could fall further. And there is continued concern about the impact of the war in Ukraine.

But if rising interest rates succeed in controlling inflation and geopolitical uncertainty eases, there could be better news for investors.

Given the current volatility of stock markets, it may be worth considering some of the following steps to protect portfolios against a downturn:

(i) Diversify into different sectors and countries

Collective investment products such as funds and investment trusts offer a ready-made, diversified portfolio of share-based assets. This is a lower-risk option than investing directly in individual companies.

Buying funds covering different geographic or industry sectors will reduce volatility and the risk of one or more sectors underperforming. Legendary investor Sir John Templeton extolled the virtue of diversification, saying that “The only investors that don’t need to diversify are those that are right 100% of the time.”

As finance expert Tony Featherstone states in ASX Investor Update: “Income investing is about more than yield. It’s also about managing risk by building and maintaining a diversified portfolio across asset classes. This is especially important for older investors, such as retirees, who want income and capital stability.”

(ii) Diversify into different assets

Which brings us to diversification into non-equity-based assets, such as bonds, property and commodities, that may also protect your portfolio in the event of a stock market crash.

It’s important to pick assets that aren’t correlated, in other words, their price movements do not move up and down together, but rise and fall at different times. That way, if one asset falls in value, this should hopefully be offset by other assets holding, or increasing, their value.

For example, while North American equity funds achieved the highest returns in both 2019 and 2020 amongst this group, the sector has delivered a negative return in the year-to-date.

Diversifying into commodity, infrastructure and property funds would have allowed investors to offset negative returns from equities in 2022 against the positive returns in these sectors in both 2021 and 2022 (to date).

If you are looking for a low-cost way to diversify, then there are a number of Exchange-Traded Funds (ETFs) that track the prices and/or indices of certain asset classes, including commodities. Most ETFs in Australia are passive investments, and don’t try to beat the market. ETFs track a range of asset classes, including precious metals and commodities, bonds, crypto, foreign currencies, as well as of course local and international shares.

(iii) Timing your investments

It is very difficult to buy low/sell high when markets are volatile or a crash is imminent. However, there are still steps you can take in terms of timing your investments.

One option is to invest monthly, rather than as a lump-sum, allowing you to benefit from ‘dollar cost averaging’. This means that, if stock markets and share prices fall, investors are able to buy more shares or units for the same amount. As a result, investors end up paying the average price across the whole period.

As discussed earlier, investing for the long-term (at least 10 years) helps investors to protect against the impact of stock market crashes.

(iv) Consider your super fund exposure

The Federal Government’s Moneysmart site, recommends that your choice of superannuation be tailored to your risk appetite, age, and how long before you will be able to access the funds. For example, it’s common for Australian workers in their 20s and 30s to opt for growth superannuation funds, with high exposure to shares, because if the stock market crashes they have time to regain the money before they retire.

If you are approaching retirement however, you may opt for a balanced or conservative super fund, as they better protect you from a share market crash. For example, in a conservative fund, it is common for the investment mix to comprise of around 30% in shares and property, and 70% in fixed interest and cash. Compare this to a growth fund with around 85% in shares or property, and 15% in fixed interest or cash. A ‘high growth’ option may involve 100% exposure to shares.

As in all cases, speak with your financial advisor as to the best option for you.

(v) Other tips for protecting your portfolio

Other potential options for protecting your portfolio against a crash include:

- Stop-loss and limit orders: these allow investors to set a price at which shares are automatically sold. A stop-loss order is an order to sell shares if the price falls to, or below, a set price (the “stop” price). For example, if you bought a share costing 100 pence, and you wanted to limit your downside risk to 10%, you could set a stop-loss order of 90 pence.

- Holding cash: Of course, if you really want to ensure protection from the vagaries of the stock market then you could opt to keep your holdings in cash. Interest rates on savings accounts are low—usually below the level of inflation—however with the Big Four banks passing on rate rises to Australian mortgage holders, pressure is mounting on them to lift rates on savings products as well.

Note: When investing, it’s possible to lose some, and very occasionally all, of your money. Past performance is no prediction of future performance and this article is not intended as a recommendation of any particular asset class, investment strategy or product.

This article was written by Jo Groves and Johanna Leggatt and was originally found here: Surviving a Stock Market Crash – Forbes Advisor Australia

Recent Comments